America is draining European gold reserves – analysis

The analysis was written by Kristóf Juhász

The Trump Tariff Trade is shaking up the gold market: gold and silver bullion are now being flown on business jets from vaults in London and Zurich to the New York Commodity Exchange. This surge in transatlantic shipments could trigger a gold shortage in Europe, with the first warning signs already appearing.

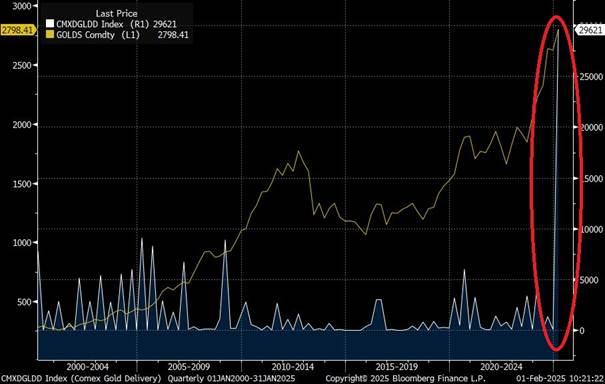

Physical gold deliveries on the COMEX futures exchange have surged to levels unseen in 25 years. In January alone, almost 3 million troy ounces (93,31 tonnes) of gold were shipped from London vaults to New York, bringing the total to 435 tonnes since Trump’s election in November, with an additional 4 million ounces (124,45 tonnes) already slated for delivery in February.

The volume of physically delivered gold (blue, right scale, 100 ounces) and gold price (yellow line, left scale, USD/ounce) on COMEX from 2000 to 2025

In January 2025, a record-breaking three million troy ounces (93,31 tonnes) of physical gold was delivered to the COMEX futures exchange’s public warehouses.

The surge in physical gold deliveries is driven by arbitrage opportunities created by the price gap between the New York and London gold markets, a direct consequence of Trump’s tariff war.

The anticipated 25% tariffs on gold and silver imports from Canada, Mexico, and possibly Europe have widened the futures market premium. Consequently, gold has risen to $50 per ounce and silver to $1 per ounce over the London spot market, creating an arbitrage opportunity of approximately 1.5–3%.

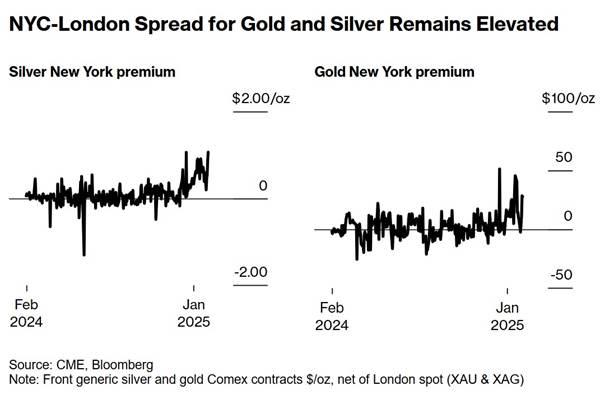

The premium difference between physical gold and silver bars between New York and London

Since Donald Trump’s election, the price spread between the London and New York precious metals markets has widened, reaching $1 per ounce for silver and $50 per ounce for gold.

This premium differential has created such a profitable arbitrage opportunity for investment banks handling multi-tonne lots that it is now more cost-effective to transport silver bullion—which is traditionally shipped by container vessel—on passenger planes from London to New York to mitigate the risks of a rapidly changing tariff landscape.

Given the weeks-long shipping time, there is a risk that the notoriously unpredictable Trump could change his stance on tariff implementation multiple times, potentially resulting in an immediate 25% loss for arbitrageurs.

According to market intelligence from Conclude Zrt – a major bullion gold dealer in Hungary – it has recently become common practice to transfer 400 oz Good Delivery gold bars from London to Zurich, where they are converted into 1 kg bars before being flown to New York to capitalize on the premium margin profit.

Dormant Frankfurt Vaults; London Running Out of Gold?

Europe’s gold trading hubs are already feeling the impact of rising U.S. gold demand. Stocks of the most popular investment gold bars and coins have been depleted in Frankfurt’s vaults, which supply EU gold traders. Meanwhile, Swiss refiners are experiencing longer production and delivery times, with some reporting pre-order waiting lists of up to 8 weeks for 1-kilo gold bars.

The LBMA responded to gold traders’ concerns about a significant decline in London’s bullion stocks with a concise statement, assuring market participants that there was “ample liquidity” to support the average daily OTC gold trading volume of $226 billion. However, this nonchalant stance contrasts with rumors, reported by Bloomberg, suggesting that gold deliveries from the Bank of England’s vaults are now delayed by several weeks.

The LBMA’s statement is meant to be reassuring:

The gold market story, which originally broke on Bloomberg, has now been picked up by Reuters. Their report indicates that not only London and Zurich, but also gold stockpiles in Dubai, Singapore, and Hong Kong—which traditionally supply precious metals to China and India—have been diverted to the U.S. in recent days. Meanwhile, there is no sign of major physical gold buybacks on the Shanghai Gold Exchange, where sales have remained steady in recent weeks, suggesting that no additional inventories are expected in the short term.

However, according to Ross Norman, managing editor of Metals Daily, concerns about London running out of gold due to rising demand are unfounded. As of December 2024, the LBMA vaults held 8,678 tonnes of gold, with 4,573 tonnes (around 400,000 bars) backing global central bank reserves stored in the Bank of England’s vaults and a further 2,912 tonnes held by physical gold ETFs, stored in various vaults throughout London. This leaves an approximate 1,193 tonnes in free floating stock, although there is no clear data on how much of this is already allocated—meaning already owned by other entities.

Update: 05.02.2025 20:05 The LBMA’s announcement originally published on 03.02.2025 has been updated to reflect that the impact of import duties on China and Hong Kong are being investigated and the reference to daily turnover coverage has been removed. LMBA also added in a more recent market update, that there is an inflow of freshly mined gold to London, amounting to 325 tonnes per month on average.

What happens if gold really does run out in Europe?

Although scenarios like this have been rare even in Conclude’s 16 years of experience, our observations during the COVID pandemic and the Russian-Ukrainian war suggest that a gold shortage could reintroduce the systemic risk premium. In other words, physical gold prices might diverge from the gold exchange rate, with physical gold trading at a significant premium over paper-based gold products—similar to what occurred in the spring of 2020 and 2022.

It is also possible that this is the early stage of a large-scale market cornering speculation, designed to exploit the price gap between physical gold and futures contracts. This potential scenario has been highlighted by gold traders in the U.S., London, and Hong Kong—each with nearly four decades of experience—who have shared their insights with Conclude.

In Conclude’s view, the spike in physical gold demand loco London may be just a one-off arbitrage opportunity that will gradually fade over time, allowing the market to return to its slow but steady upward trend. This comes as gold reached a new all-time high of $2,940/oz in February.

One thing is certain: free floating stocks of physical gold are inherently limited, unlike the unlimited supply of money printed without inhibitions since the 2008–2009 global financial crisis. If demand for physical gold suddenly surges, those who wait for a full-blown market panic before buying investment gold may find themselves left empty-handed.